Latest financial prices as of : Prices fluctuate up away from 6.1% again

Glen Luke Flanagan try good deputy publisher at the Chance Advises exactly who targets financial and you may credit card blogs. Their prior roles were deputy editor ranks at the Usa Now Strategy and you will Forbes Advisor, and senior blogger during the LendingTree-the worried about credit card rewards, fico scores, and relevant information.

Benjamin Curry ‘s the manager regarding content at the Fortune Recommends. With well over 2 decades of news media experience, Ben have commonly protected monetary locations and private money. In earlier times, he was a senior publisher during the Forbes. Just before one to, the guy worked for Investopedia, Bankrate, and you may LendingTree.

The modern average rate of interest to possess a fixed-speed, 30-seasons compliant mortgage in the usa was 6.127%, with regards to the current analysis provided by financial tech and investigation business Optimum Bluish. Read on to see average costs for various form of mortgages as well as how the current rates compare to the final advertised big date earlier.

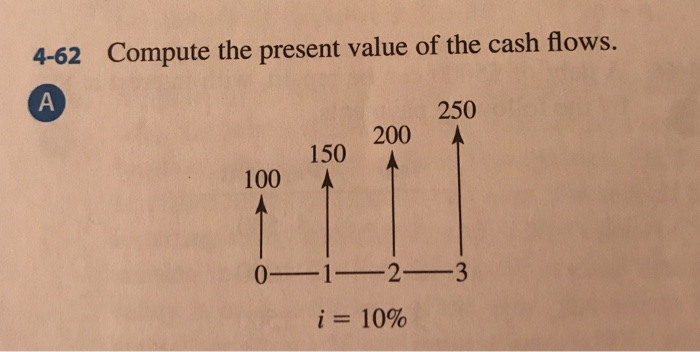

Historical financial prices graph

Mention, discover a lag of just one working day within the investigation reporting, which means most current speed as of today is what the graph reveals to possess September 26.

30-season compliant

The typical interest rate, for every one particular most recent study available as of this composing, are 6.127%. That’s right up regarding 6.077% the past stated big date previous.

30-year jumbo

What’s a jumbo home loan otherwise jumbo mortgage? This basically means, they is higher than the maximum amount having a regular (conforming) mortgage. Fannie mae, Freddie Mac, plus the Government Homes Loans Company set it restriction.

An average jumbo home loan speed, each more latest data offered during this composing, is actually 6.429%. Which is right up from 6.417% the last stated go out past.

30-12 months FHA

The Government Casing Government brings home loan insurance to specific loan providers, while the lenders therefore could offer an individual a better contract towards issues such as for instance having the ability to be eligible for a good home loan, potentially and make an inferior advance payment, and possibly bringing a lowered speed.

The average FHA financial rates, for each the quintessential latest investigation readily available at the creating, is actually 5.875%. That’s right up regarding 5.818% the final advertised day previous.

30-12 months Va

A beneficial Va mortgage exists by a private financial, nevertheless Company out of Experts Circumstances pledges section of it (cutting exposure into the bank). They are obtainable if you find yourself a great You.S. military servicemember, an experienced, otherwise an eligible enduring mate. Such financing get either allow purchase of a property with no advance payment at all.

The common Va home loan rate, for each and every probably the most latest analysis offered during this creating, is 5.579%. That is upwards from 5.510% the final said day early in the day.

30-seasons USDA

This new U.S. Department out-of Farming works software to help reasonable-earnings applicants go homeownership. Instance funds can help U.S. owners and you may qualified noncitizens pick a house with no downpayment. Keep in mind that there are stringent requirements so that you can meet the requirements having a USDA mortgage, instance money constraints and also the domestic in an eligible rural town.

The average USDA financial rates, per the absolute most newest analysis offered at this creating, are 5.982%. That is down away from 5.987% the last advertised time early in the day.

15-seasons financial pricing

A 15-seasons financial usually generally speaking suggest large monthly payments however, reduced focus paid back across the lifetime of the borrowed funds. The typical rate to own an effective 15-season conforming financial, for every single one particular most recent study offered only at that creating, is actually 5.304%. That is upwards of 5.224% the very last stated time past.

How come home loan pricing changes many times?

Your credit history greatly affects the mortgage rates, however, you will find external affairs at the play too. Key factors become:

- Federal Set-aside decisions: In the event that Federal Set aside changes the government loans rate, loan providers normally adjust their interest costs responding. This action facilitate new Provided perform the bucks also provide, affecting credit costs for consumers and you may organizations.

- Rising prices style: Regardless if connected, inflation and Fed’s methods was separate activities. Brand new Provided adjusts rates to deal with rising prices, whenever you are lenders you are going to on their own increase prices to keep profits throughout high inflation periods.

- Monetary circumstances: paydayloanalabama.com/fort-payne Lenders envision things like financial growth and you may property supply and you may consult when means home loan rates. These are simply two the many issues that may determine price transform.

And therefore mortgage is best for your?

There is no universal solution to an informed variety of mortgage. Although many mortgage loans are antique, government-backed loans you will offer a less expensive way to homeownership to own accredited someone.

Jumbo mortgages try suitable for to invest in pricey belongings that surpass conforming loan constraints, but they tends to be costlier in the long term.

Adjustable-price mortgage loans (ARMs) basically start with reduced cost that will raise throughout the years. Weigh this cautiously based on debt agreements.

If the price hunting seems daunting, a large financial company will assist (to possess a charge) to find a knowledgeable home loan provide according to your circumstances.

How high enjoys financial pricing held it’s place in going back?

When you are financial costs may suffer heavens-higher these days compared to sub-3% prices certain homebuyers scored into the 2020 and you may 2021, what our company is viewing currently is not that uncommon when compared with historic research on home loan price averages. Listed here are two charts on the Government Put aside Monetary Study (FRED to have quick) on the internet database to own perspective.

30-year fixed-price home loan historical trends

If you believe cost ranging from six% and you may 8% now try frightening, envision September as a result of November regarding 1981, hence spotted the common speed hanging anywhere between 18% and you will 19%, according to FRED.

15-season repaired-price financial historical fashion

Pricing now into fifteen-year mortgage loans, as revealed in the Max Blue investigation a lot more than, try more or less into the level if you don’t slightly below that which we look for through the of many earlier in the day symptoms. Such as, glance at FRED study to your stop from 1994 and start of 1995, when prices neared nine%.

Laisser un commentaire