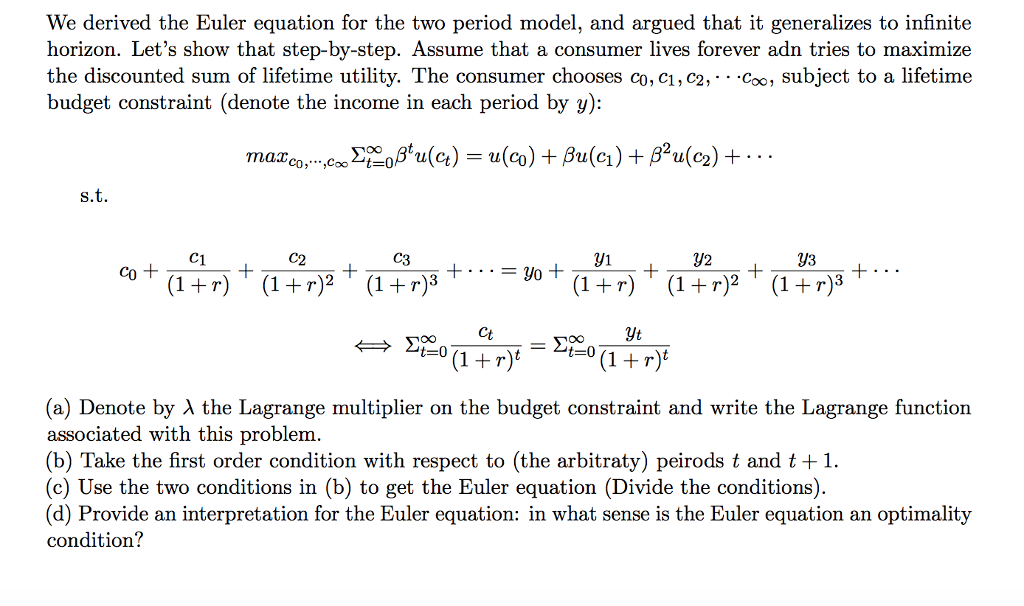

Allow your House Look after You which have a face-to-face Mortgage/ Domestic Security Conversion Mortgage

A contrary home loan is a non-recourse loan, which means that brand new debtor (or even the borrower’s estate) from an opposing financial does not owe more the future loan balance and/or value of the home, whichever is actually smaller. In the event the borrower or agencies of their estate favor to offer the house to pay off the reverse home loan, no assets apart from the house would-be regularly pay your debt. When your borrower or their unique estate would like to maintain the home, the balance of one’s financing have to be paid in full.

Opposite mortgage loans are manufactured particularly for older homeowners, permitting them to make use of this new collateral he’s got obtained within their land.

That have an opposite home loan, your borrow on the fresh new collateral you have established in your property and do not need pay back the borrowed funds as long because you reside in your house as your no. 1 house, keep house within the good shape, and you can shell out possessions fees and insurance. You might live in your residence and revel in and come up with zero month-to-month prominent and you may desire mortgage payments.

Based on your financial situation, an other mortgage contains the potential to make you stay inside your property and still fulfill debt loans.

We all know one to opposite mortgage loans may not be right for folks, call us so we might help http://www.availableloan.net/payday-loans-in/hudson/ take you step-by-step through the procedure and you may answer any questions you’ve got.

Contrary Mortgage loans versus. Traditional Mortgage otherwise Domestic Equity Financing

A reverse financial ‘s the opposite of a classic mortgage. Which have a classic financial, you borrow cash making month-to-month dominant and focus mortgage payments. That have a reverse home loan, but not, you get mortgage proceeds in accordance with the value of your house, age the latest youngest debtor, therefore the rate of interest of one’s mortgage. That you do not create monthly principal and you will focus home loan repayments for if you live in, maintain your home during the great condition, and you may spend property taxation and you may insurance rates. The borrowed funds have to be reduced after you perish, sell your residence, if any longer inhabit your house since your no. 1 quarters.

While you are ages 62 or old, a property Equity Conversion process Financial (HECM) to buy away from Lender from The united kingdomt Home loan could be an intelligent option for resource a special spot to phone call household.

Home Collateral Conversion Mortgage (HECM) A property Guarantee Conversion process Mortgage, or HECM, ‘s the simply reverse home loan covered because of the U.S. Government, that’s only available using an FHA-recognized financial.

In place of being forced to search old-fashioned capital, individuals age 62 and you may elderly should buy a new home if you’re eliminating mortgage repayments* as a consequence of an opposite mortgage (However, they will still be responsible for spending possessions taxes and you may needed homeowners’ insurance). This may help them more conveniently afford an improvement, otherwise spend less money away-of-pocket. Retiring Boomers are choosing to keep a gentle existence in the an effective family one finest suits their requirements. You possess the house, together with your term on the label and the home get and an opposing financial closure try rolled towards the you to, and also make your own processes much easier.

Just how much Are Borrowed?

Generally, the greater amount of your home is really worth, the newest elderly youre, as well as the lessen the interest, the more you will be able so you can obtain. The maximum amount which can be borrowed to your a particular mortgage system is founded on these things:

- Age the youngest borrower in the course of brand new financing.

- The new appraised property value the home.

- Most recent Interest rates

Initially Qualifications Standards for Opposite Mortgages

- Property owners must be 62 years old or old and inhabit the house or property as his or her primary residence

- The house ily or a two-4 Product possessions, Townhome, otherwise FHA-recognized Condo

- Your house need to satisfy lowest FHA assets standards

- Debtor cannot be unpaid to your people federal financial obligation

- End away from HECM counseling

All of the money try subject to borrowing recognition together with credit worthiness, insurability, and you may ability to give appropriate collateral. Not absolutely all finance otherwise items are available in most of the states otherwise counties. An other home loan is financing that needs to be paid off whenever the home is no longer the primary residence, is available, or if perhaps the property taxes or insurance rates aren’t reduced. That it mortgage isnt a federal government work for. Borrower(s) have to be 62 or old. Our home need to be maintained to satisfy FHA Conditions, and also you have to still pay possessions fees, insurance and you will property related charge or else you will clean out your house.

Laisser un commentaire